Linear Programming Code

All the code is written in matlab. Please visits here for a complete version of my code. The code base is in reference to Dr. Chunming Wang's MATH467 project code.

1. Implementation of the basic simplex algorithm

Code

function [Solution,BasicVar,Status] = AxEqualsb(A, b, c, BasicVariables)

[rows, ~] = size(b);

if (all(b >= 0) && rank(A)==rows)

[Solution,BasicVar,Status]=basicsimplex(A,b,c,BasicVariables);

else

disp('b must be nonnegative and rank(A) == size of b');

end

end

Interpretation

- The function works for Contraint .

- It checks whether is non-nagative using

all(b >= 0). - It also checks the matrix is full rank using

rank(A)==rows. - If all the inputs are valid, we feed all the parameters into the

basicsimplex()function and return the results.

Results

I use the following code to test the algorithm. I set A = [[1,0,1];[0,1,1]], b = [1;2], and c = [-1;-1;-3].

The result I expected to get is [0;1;1].

Running this to test:

A = [[1,0,1];[0,1,1]];

b = [1;2];

c = [-1;-1;-3];

[Solution,BasicVar,Status] = AxEqualsb(A, b, c, [1, 2])

Solution =

0

1

1

BasicVar =

3 2

Status =

0

We can see the basic variables are and with values and respectively. Status = 0 showing the results are valid.

2. Implementation of general linear programming algorithm

Code

function [Solution,BasicVar,Status] = AxSmallerThanb(A_hat, b_hat, c_hat)

[rows, ~] = size(b_hat);

if (all(b_hat >= 0) && rank(A_hat)==rows)

I = eye(rows);

c_new = [c_hat;zeros(rows,1)];

A_new = [A_hat I];

[~, A_cols] = size(A_hat);

BasicVariables = (A_cols+1):(rows+A_cols);

[Solution,BasicVar,Status]=basicsimplex(A_new,b_hat,c_new,BasicVariables);

else

disp('b_hat must be nonnegative and rank(A) == size of b_hat');

end

end

function [Solution,BasicVar,Status] = AxGreaterThanb(A_tilda, b_tilda, c_tilda)

[rows, ~] = size(b_tilda);

if (all(b_tilda >= 0) && rank(A_tilda)==rows)

I = eye(rows);

A_phaseII = [A_tilda -I];

c_phaseII = [c_tilda;zeros(rows, 1)];

A_phaseI = [A_phaseII I];

[~, A_cols] = size(A_tilda);

PhaseI_BasicVariables = (A_cols+1+rows):(2*rows+A_cols);

c_phaseI = [zeros(A_cols+rows, 1);ones(rows, 1)];

[SolutionI,BasicVarI,StatusI]=basicsimplex(A_phaseI,b_tilda,c_phaseI,PhaseI_BasicVariables);

if (StatusI==0)

% Phase II

[Solution,BasicVar,Status]=basicsimplex(A_phaseII,b_tilda,c_phaseII,BasicVarI);

else

Solution=SolutionI;

BasicVar=BasicVarI;

Status=StatusI;

end

else

disp('b_tilda must be nonnegative and rank(A) == size of b_tilda');

end

end

Interpretation

- The first function

AxSmallerThanb()works for Contraint .- It checks whether is non-nagative using

all(b >= 0). - It also checks the matrix is full rank using

rank(A)==rows. - If all the inputs are valid, we are going to add slack variables to make the problem standard.

- Finally, we feed all the parameters into the

basicsimplex()function and return the results.

- It checks whether is non-nagative using

- The second function

AxGreaterThanb()works for Contraint .- It checks whether is non-nagative using

all(b >= 0). - It also checks the matrix is full rank using

rank(A)==rows. - If all the inputs are valid, we are going to first add slack variables to make the problem standard, and call it

A_phaseII. - Second, we are going to add phase I variables so that we have an intial basic solution.

- Third, change the objective function based on the phase I variables .

- Next, we feed all the parameters into the

basicsimplex()function and return the results. - Then, do phase II simplex method based on the

BasicVarIreturned from phase I. - Finally, the results are returned.

- It checks whether is non-nagative using

Results

I'm going to use the same , , and as part 1.

Running this to test:

[Solution,BasicVar,Status] = AxSmallerThanb(A, b, c)

[Solution,BasicVar,Status] = AxGreaterThanb(A, b, c)

Solution =

0

1

1

0

0

BasicVar =

3 2

Status =

0

Solution =

0

0

2

1

0

BasicVar =

4 3

Status =

-1

- We can see for the first case, the basic variables are and with values and respectively.

Status = 0showing the results are valid. - For the second case, it's straightforward that the solution will be infinity. Indeed,

Status = -1proves that there's no solution for this case.

3. Study of versus approximation

Code

% Part 3 Apple stock vs Dow Jones Index

Apple = readtable('APPL_DATA.csv');

Apple = flipud(Apple);

Apple = Apple(1:253,[1,4]);

Apple = table2array(Apple(:,2));

DowJones = readtable('Dow_Jones.csv');

DowJones = DowJones(:,1:2);

DowJones = table2array(DowJones(:,2));

DowJones = str2double(DowJones);

X = transpose(DowJones)

Y = transpose(Apple)

n = 253;

% L1 Regression

[RegressionModel]=L1_MultilinearRegression(X,Y);

%

% Least square

%

Xhat=X-mean(X,2)*ones(1,n);

Yhat=Y-mean(Y);

Coef_LSQ=inv(Xhat*Xhat')*Xhat*Yhat';

Intersect_LSQ=mean(Y)-Coef_LSQ'*mean(X,2);

Prediction=Coef_LSQ'*X+Intersect_LSQ;

%

figure;

plot(Y,RegressionModel.Prediction,'o','MarkerSize',[8],'MarkerFaceColor','r','MarkerEdgeColor','r');

hold on

plot(Y,Prediction,'o','MarkerSize',[8],'MarkerFaceColor','b','MarkerEdgeColor','b');

%

figure;

plot(Y'-RegressionModel.Prediction,'o','MarkerSize',[8],'MarkerFaceColor','r','MarkerEdgeColor','r');

hold on

plot(Y-Prediction,'o','MarkerSize',[8],'MarkerFaceColor','b','MarkerEdgeColor','b');

RegressionModel.SRE

sum(abs(Y-Prediction))

Explanation

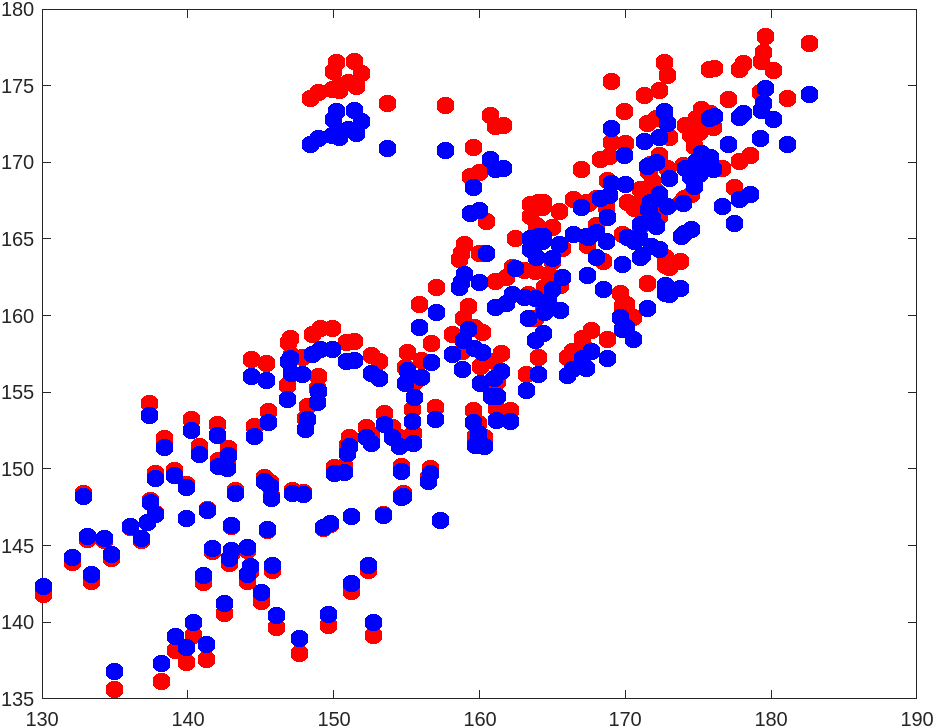

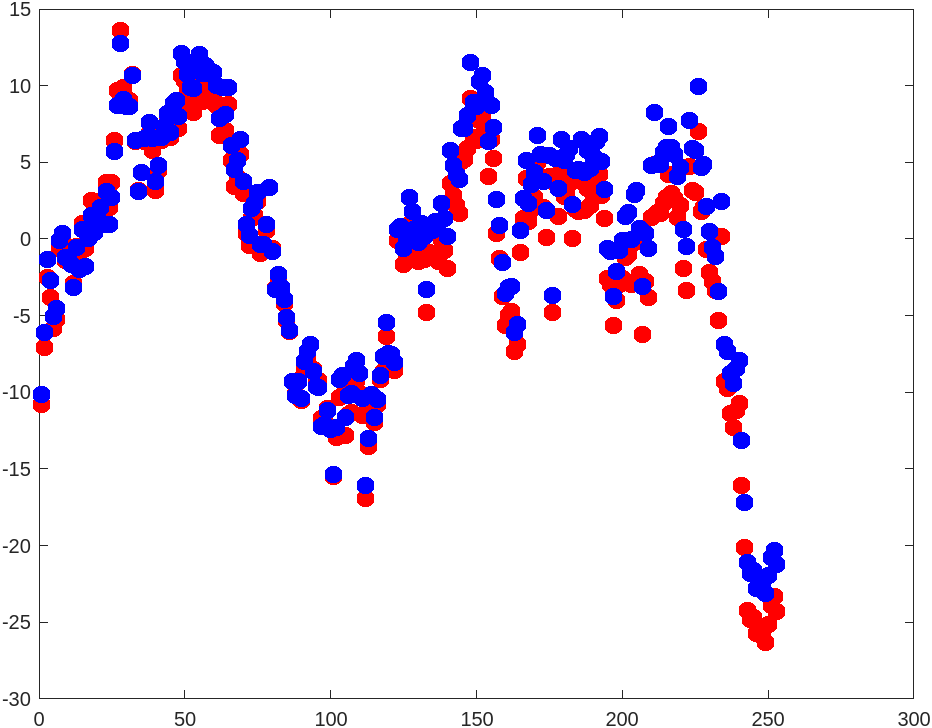

- For this part of the problem, I'm using Apple Stock Price data and Dow Jones Index Price data for the past year.

- First, I read the data from the

.csvfiles and do some manipulations to them to a vector. - Second, I feed both data into

L1_MultilinearRegression(X,Y),Xis Dow Jones data andYis Apple data. This should return a model. - Third, I perform regression on the same set of data.

- Close to finish, I plot the regression model and the residual graph for both types of regression, shown in figures below.

- Finally, I return the sum of residuals for both models.

Results

Figure for regression model:

Figure for residual plot:

Sum of residuals (first one is for , second one is for ):

ans =

1.5284e+03

ans =

1.5824e+03

Comparison of Results

The sum of residuals is a little higher than the sum of residuals. We also discover that typically guards against severe mistakes. The red dot in the picture above, which reflects predictions, is visible more frequently in areas farthest from . This is due to the tendency of regression to punish extreme spots (projections represented in blue dot).